Advertisement

OPINIONS

SEA Limited A Good Buy? Garena, Shopee, SEAMoney (FINANCIAL HORSE)

With SEA surging past $200, is it too late to get in on the action?

Financial Horse is a leading investment site in Singapore, check out Financial Horse's Guide to Investing.

What's new?

MAS announced on Friday (Dec 4) that it will award digital full bank licences to the Grab-Singtel consortium and tech giant SEA!

Singapore will thus have 4 digital banks, with Grab-Singtel and Sea getting digital full bank licences.

Why do we care?

SEA Limited has had an incredible run in the stock markets this year. Over 300% increase in 2020 alone.

SEA's market cap today of US$92 billion is twice that of DBS, and triple that of Singtel. Crazy stuff right?

Is SEA Limited Over-Valued?

Before we can answer this key question, let's delve into some fundamentals.

What is SEA? – Garena, Shopee and SeaMoney

Sea operates three key businesses:

Garena (gaming),

Shopee (eCommerce), and

SeaMoney (Fintech).

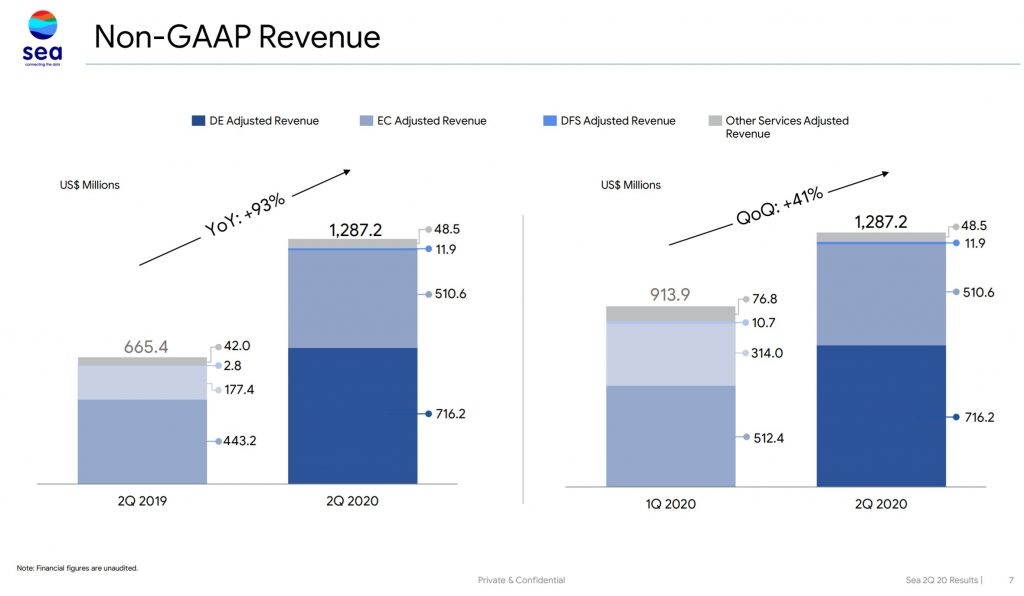

Revenue breakdown of Sea

Revenue charts are set out below, and the biggest revenue generator is Garena, followed by Shopee. The Fintech arm is still very small for now, but it does hold a lot of promise.

Sea doesn’t break down profit numbers by segment, but based on their prior statements:

Garena is by far the main profit generator, and within Garena most of the profits comes from a few top games like Garena Free Fire (a Battle Royale like PUBG for the gamers).

Shopee is still in the money burning stage, so it doesn’t make profits. Rather, it burns a ton of cash.

In short, Sea is today, is a gaming and ecommerce business, with the former generating the bulk of the profits. There is also a fintech arm they plan to grow strongly in the coming years, especially with their newly minted Digital Bank License.

Want more insightful market commentary? Subscribe to Financial Horse's 2021 Stock Watch!

Bull Case for Sea

The bull case is easy to see. South East Asia is one of the fastest growing regions in terms of economic growth.

At the same time, Sea is exposed to gaming, eCommerce and fintech, in a region where the digital (and physical) infrastructure so far has been very undeveloped, and where competition isn’t crazy intense like US or China. In some ways, it feels like China in early 2010s, before the Tencent and Alibaba became who they are today.

Valuations

Let’s run some simple valuations to answer – how much is Sea worth if they become Alibaba / Tencent for South East Asia?

If we assume Sea can one day become as dominant as Alibaba / Tencent in South East Asia, it’s valuation can probably double from here.

But that’s a big IF, because South East Asia is a very different market from China.

South East Asia is disparate (not homogenous market like China)

eCommerce penetration in China is way higher

Alibaba / Tencent are more dominant

What are the risks with Sea?

Garena (Gaming)

2 big risks:

Gaming drives the bulk of the profits for now, driven by a few games

In 2019, Garena's top five games, which included Free Fire, contributed 94.5% of our digital entertainment revenue.

Gaming is a fickle business. So a game may lose popularity over time, and then you’ll need to find new games.

Sea doesn’t own many of the most popular games, other than Garena Free Fire. They simply own the distribution rights. So for now, they’re pretty beholden to Tencent. Fortunately, Tencent is a big shareholder.

Shopee (Ecommerce)

This one is simple – competition.

The biggest competitors in South East Asia will be Lazada, Tokopedia (for Indo) and Qoo10/Carousell (for Singapore). Lazada, Qoo10, and Tokopedia are all very strong contenders, with Lazada particular challenging given their Alibaba financial backing and expertise. And don’t forget the dark horse Amazon as well.

SeaMoney (Fintech)

SEA has gotten approved for a digital bank licence in Singapore, and with their strong track record of execution, I’m pretty excited to see what they do with it.

That said, the competition will likely be very intense. Not only do you have the established banking sector to contend with (DBS, OCBC, UOB), you also need to fight the fintech players (Grab, Bytedance etc).

Shareholders of Sea

2 big shareholders: (1) the founder, Forrest Li, and (2) Tencent.

I like it when the founder has a big stake and is actively involved in the day to day, I think that’s crucial to the success of any company.

I also really like the Tencent backing, because that opens a lot of doors, and a lot of games, for Sea.

Putting everything together

The way I see it, I really like the space Sea is in – South East Asia, eCommerce, Gaming, Fintech.

All areas with lots of growth in the coming decade.

I also really like Sea’s execution, I think they’ve executed unbelievably well in eCommerce and gaming. And I’m excited to see what they can do with a digital banking licence.

But at the same time, South East Asia is not China. The people are less affluent, and it’s a very disparate bloc, with differing consumer tastes and regulations. It’s also why Shopee decided to split their app and have different teams and tailored strategies for each country.

The problem with this though, is that it may mean Sea may never achieve the kind of margins that Tencent / Alibaba can in China, because costs will never be as competitive.

And realistically, there’s also a lot of competition, in each of the verticals Sea is in. Gaming is the big money spinner now but that can change quickly, and neither Garena nor Shopee has the kind of dominance of Wechat or Taobao just yet.

At the end of the day, the stock has gone on a 200%+ increase the past 6 months. That’s a lot of growth priced in, and the slightest misstep at this level can trigger a sell-off.

Covid lockdowns were a great boost for eCommerce and Gaming, but as South East Asia starts to reopen again, some of the growth might start to slow.

My personal view here is that some of the price increase might have gotten ahead of itself, at least short term. There could be a possibility of a near term correction.

Long term wise, I do still like the prospects of this company.

I’ll give Sea a 3.5/5 Financial Horse rating.

Would love to hear what you think about SEA. Share your comments below!

Sea Limited – Financial Horse Rating

3.5/5

For more Investing Content, check out Financial Horse's Youtube Channel!

Comments

2195

0

ABOUT ME

Financial Horse was started to demystify financial investments.

2195

0

Advertisement

No comments yet.

Be the first to share your thoughts!