Advertisement

OPINIONS

One of the best banks in Singapore: DBS Bank

DBS Stock Analysis

DBS provides a variety of commercial banking and financial services, mostly in Asia. Consumer Banking and Wealth Management, Institutional Banking, Treasury, and others are among the company’s operational segments.

Back in 2020, DBS, or indeed the whole Singapore market, took far longer to recover than its counterparts in the United States. Because interest rates are near 0%, the prognosis for DBS becomes hazy. The Monetary Authority of Singapore (MAS) has also requested that Singapore banks pay lower dividends to shareholders in order to buffer capital during the COVID-19 issue, which may turn off potential investors.

DBS Bank, the darling among Singapore’s major banks (UOB and OCBC), is extremely dear to every Singaporean’s heart. This is because, for the majority of us, the first bank account we may open is, more often than not, a DBS account. Moreover, DBS is a state-owned bank. With over 28.9% of DBS shares owned by Temasek Holdings, Singapore’s 2nd largest sovereign fund. Hence, DBS tends to have a greater valuation than the other two banks.

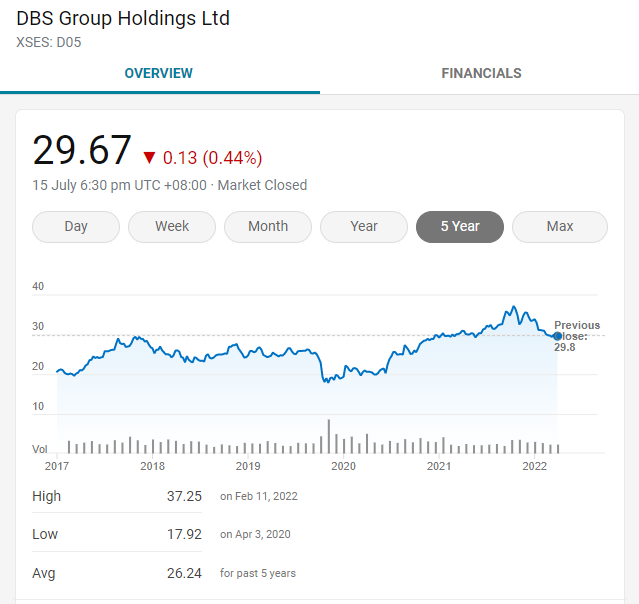

With DBS down 20% from this year’s peak in February this year till today due to the uncertainty in the market. I am intrigued to discover more about DBS and whether this could be a good opportunity to start buying shares of DBS. Let’s now take a look at what DBS has to offer.

An Overview of DBS’s Business

1. Key Product & Services under DBS

The 3 main operating segments that constitute the Total Interest Income are: Net Interest Income, Fee Income and Non-Interest Income.

Qualitative Factors affecting DBS

Let’s now take a deeper look into the qualitative aspects that affect the business.

Growth Opportunities for DBS

1. Rising Interest Rate Environment

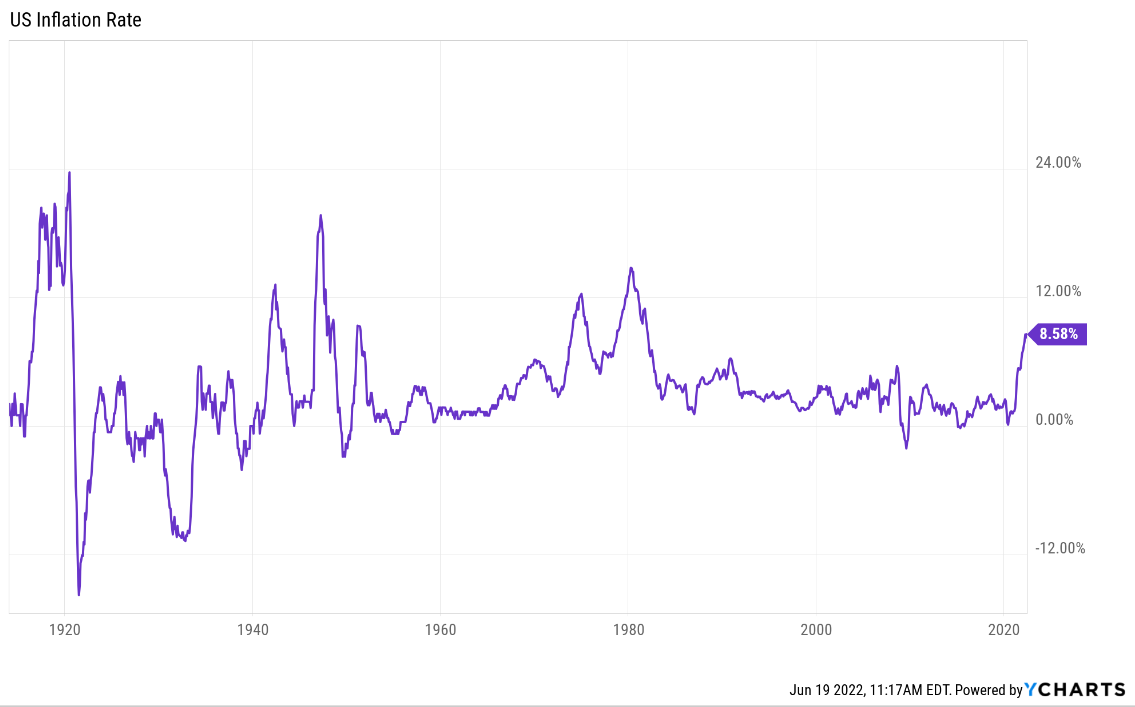

In May 2022, inflation reached 8.58%, its highest level in 20 years. To avoid hyperinflation, the Federal Reserve Board (Fed) must raise interest rates in order to cool an overheated economy and lower inflation. The latest 0.75% (during June) increase in interest rates was the greatest since 1994, when the rate was 1.75% at the time of writing (19th June 2022). DBS will gain from this climate since increasing interest rates will allow them to charge higher interest rates on variable loans. These are important to banks, like DBS, since they are how they generate net interest revenue for their total income.

2. Moving Digital

DBS is putting a greater emphasis on digitalization. Some of its new endeavors, such as the Digital Exchange, are intriguing but little in comparison to the bank’s primary economic interests. To remind readers, this is a cryptocurrency exchange platform, like bitcoin.

However, one of the primary reasons for DBS’ success thus far and why they will continue to do well in the future is that they are one of the most digitally advanced banks in the world, and they continue to invest and innovate to preserve this lead. DBS’ digital clients make four times the revenue and cost much less, making everyone they acquire significantly more profitable.

Business Risks for DBS

1. Heightened macroeconomic and geopolitical risks

Unfortunately, the regulatory environment had a negative impact on DBS, making it difficult for them to operate throughout the previous decade. DBS is actively seeking new opportunities and is fortunate to have made significant advances through three transactions – Lakshmi Vilas Bank (LVB) in India, Citigroup’s consumer banking business in Taiwan (Citi Consumer Taiwan), and Shenzhen Rural Commercial Bank (SZRCB), which will position DBS well for growth over the next decade.

DBS anticipates that these deals will contribute around SGD 1.2 billion – 1.3 billion to their revenue and an additional SGD 0.5 billion to their bottom line by 2024. However, due to the conflict in Ukraine and Russia, as well as supply chain concerns throughout the world, these estimates remain uncertain. Furthermore, in Asia, the relationship between China and Taiwan appears to be deteriorating, which might have serious consequences if China decides to “reunify” with Taiwan.

2. Credit Risks

Credit risk remained the most important risk for DBS in 2021. COVID-19 had a significant influence on several of these customers in the aviation and hospitality industries. Furthermore, the interest rate is expected to rise in the following months in order to combat inflation. Such clients may have to scale an even higher mountain. Furthermore, there is a chance that clients will over-leverage themselves today since they did not consider the growing interest rate when taking out a loan. These clients will need to be recognized sooner since there might be a domino effect in times of uncertainty.

While DBS does an excellent job of managing such clients, credit risk is likely to be the most significant and emerging risk among the others.

Quantitative Factors affecting DBS

Let’s now take a deeper look into the quantitative aspects that affect the business.

1. Financial Highlights – Total Income (Breakdown)

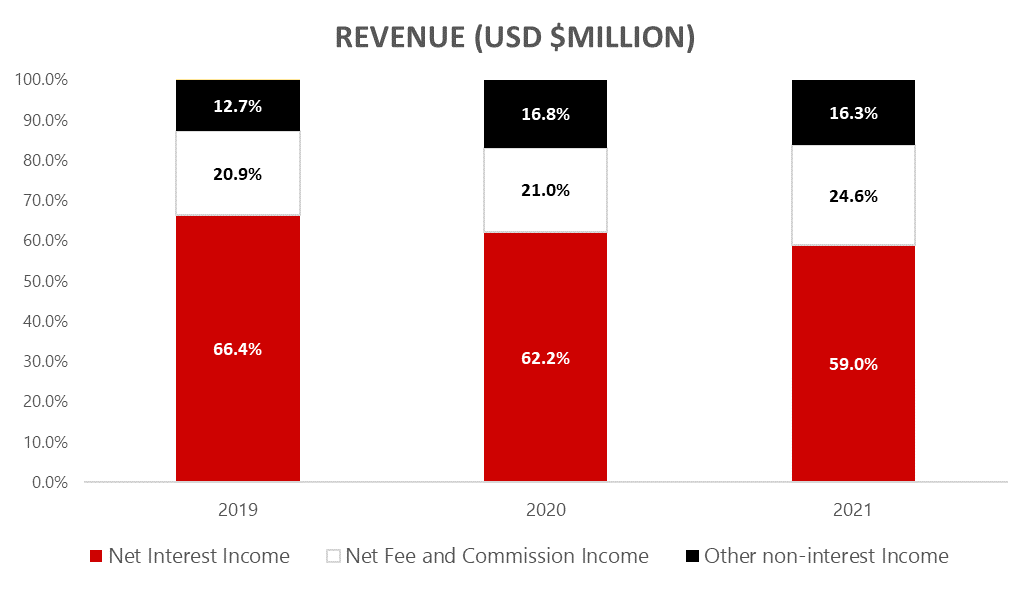

The majority of DBS’s revenue in 2021 will still predominantly come from its Net Interest Income segment, at around 60% over the last 3 years. Throughout the last 3 years, we have seen a shift of income in banks as they tide through the pandemic. Segments such as wealth management are increasingly growing as more consumers start investing in the period of 2020 and 2021. Thus, net fee and commission income increased from 20.9% in 2019 to 24.6% in 2021, while other non-interest income came in at about 16%. All the above segments were contributed by many divisions of the banks, such as consumer banking/wealth management, institutional banking, treasury markets, and others.

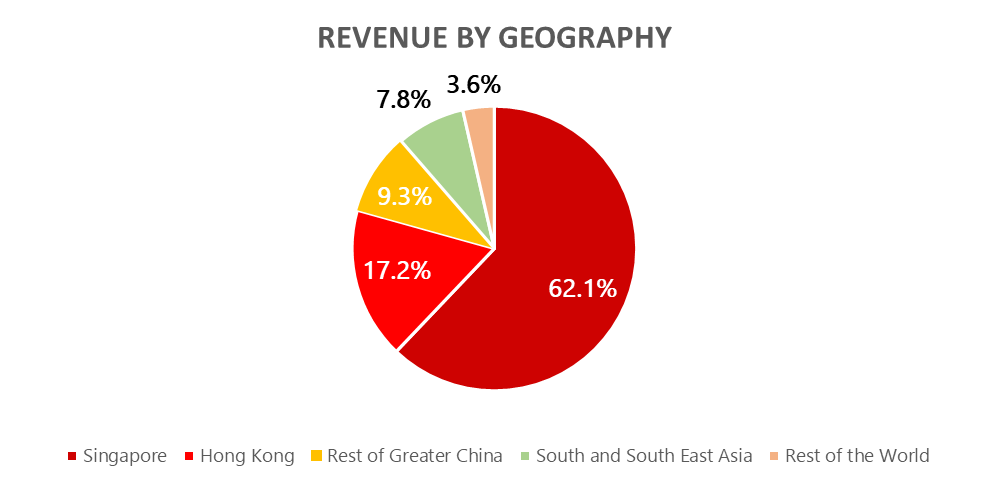

In 2021, Singapore accounted for over 62% of its revenue. Hong Kong amounted to 17.2%, 9.3% in the Rest of Greater China, 7.8% in South and Southeast Asia, and 3.6% for the Rest of the World. Singapore, Hong Kong and the rest of Greater China are impacted in total income while South and Southeast Asia and the rest of the world increase due to the 3 acquisitions made.

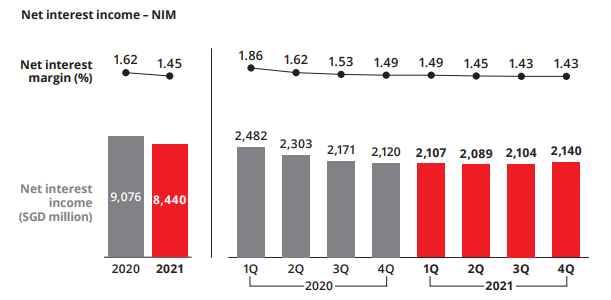

2. Net Interest Income, Net Interest Margin

Net interest income declined 7% to SGD 8.44 billion. Net Interest Margin fell 17 basis points to 1.45%. This is because benchmark interest rates used for pricing loans remained low and because of an increased deployment of surplus deposits at lower yields.

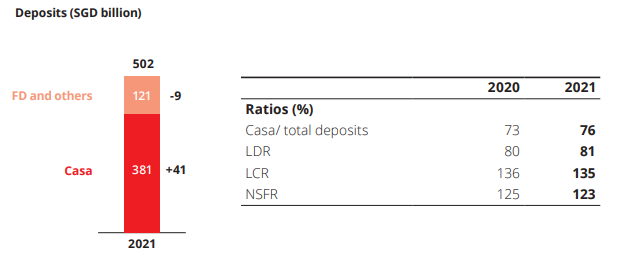

3. CASA deposits (Current Account, Savings Account)

Deposits rose by 7% to SGD 502 billion. CASA (Current Account, Savings Account) deposits grew by SGD 41 billion, enabling more expensive fixed deposits to be let go. As a result, the CASA ratio rose from 73% to 76%. Hence, DBS’s market share of total SGD deposits was maintained.

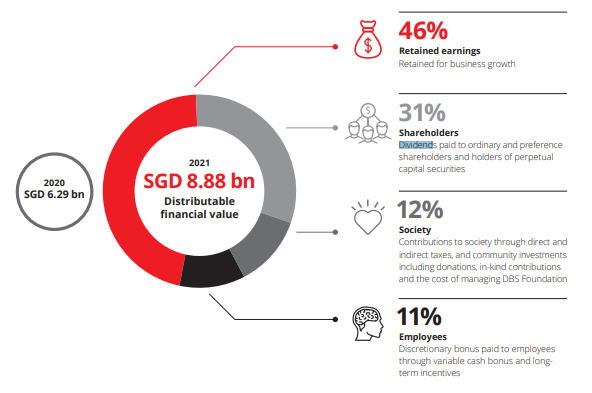

4. DBS Dividend Payout Ratio & Dividend Per Share

31% of its distributable financial value goes to shareholders paid in the form of dividends. Also, the board has proposed a final dividend of SGD 36 cents per share, which will bring the total dividend for FY2021 to SGD 1.20 per share. Barring unforeseen circumstances, the annualized dividend going forward will rise to SGD 1.44 per share, an increase of 9%.

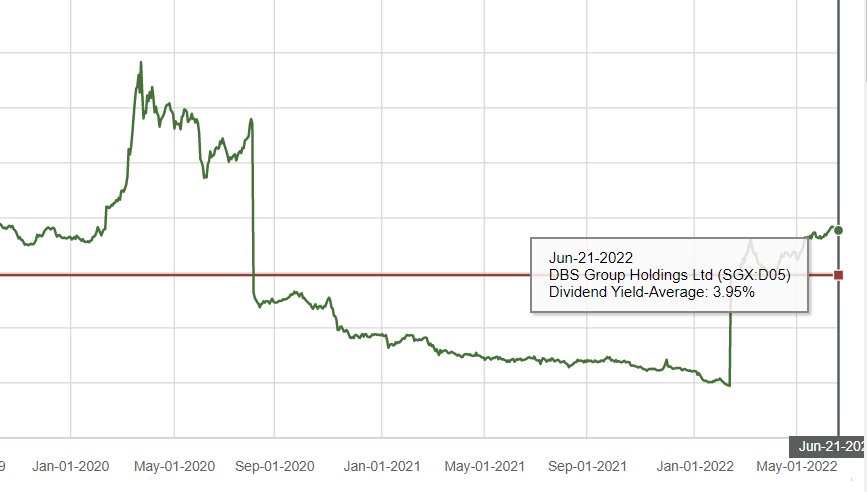

5. Dividend Yield for DBS

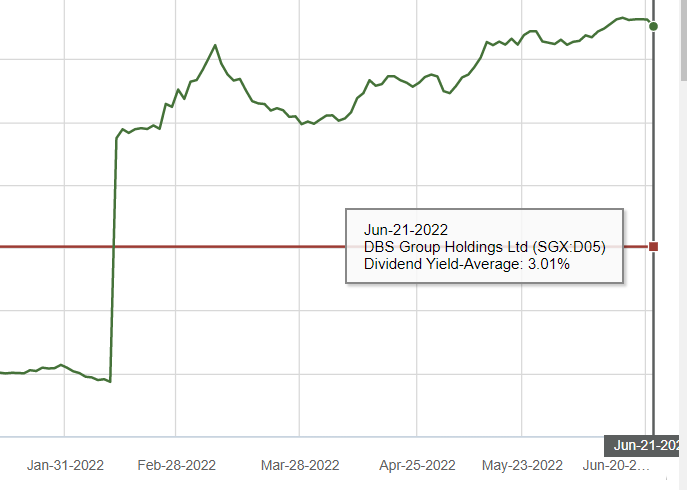

Dividend Yield (1 Year)

The current DBS dividend yield stands at 4.76%, while its 1-year average dividend yield stands at 3.01%. The sudden spike in dividend yield is due to the 4Q final dividend announcement date. Hence, the big spike.

The current DBS dividend yield stands at 4.76%, while its 1-year average dividend yield stands at 3.95%. The huge decline in dividend yield back in August 2020 was because MAS capped banks’ dividends. Thus their dividend per share was reduced to SGD 18 cents per share.

Dividend Yield (5 Year)

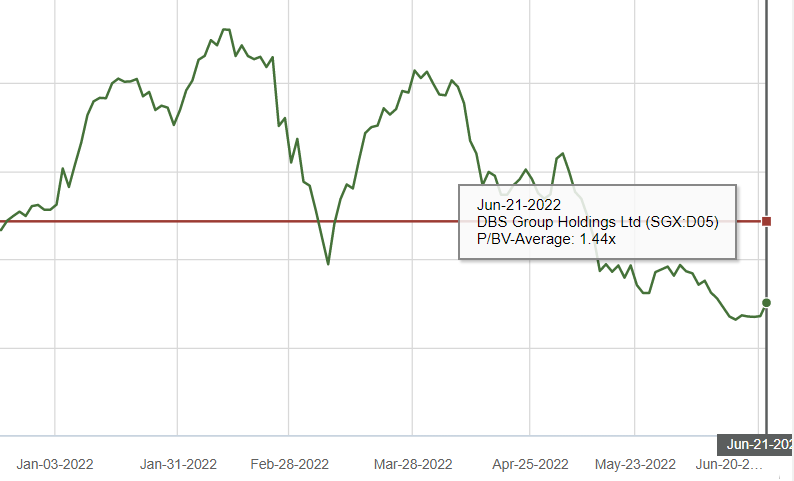

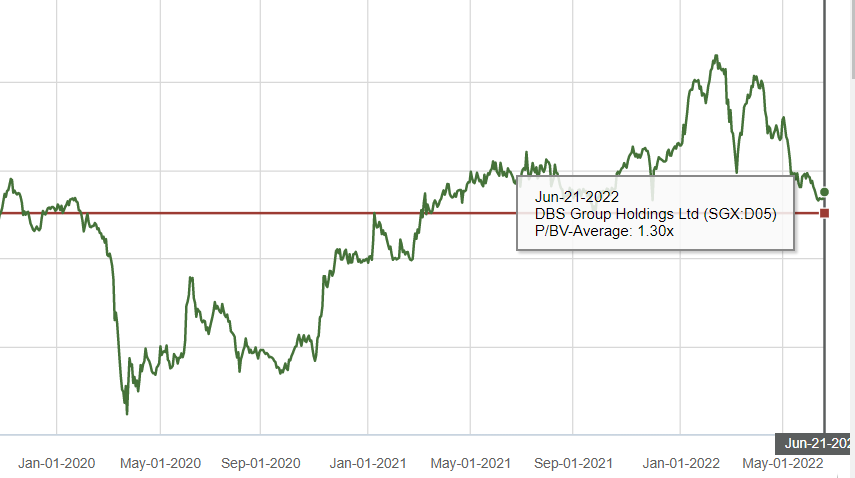

P/B for DBS

Price/Book (P/B) ratio (1 Year)

The current DBS P/B stands at 1.35x while it’s 1-year Avg P/B ratio stands at 1.44x

Price/Book (P/B) ratio (5 Year)

The current DBS P/B stands at 1.35x while it’s 5-year Avg P/E ratio stands at 1.30x

Our Stand

DBS has managed recent challenges very well, including the US-China trade war and the recent pandemic-driven downturn. Furthermore, DBS management has continued to show discipline on M&A. As well as reinvestment into growth which has shown on its financial results. Given that the outlook for DBS looks relatively optimistic:

- Interest Rate rising environment

- Focus on digitalisation

- Opportunities for M&A

DBS is trading around SGD 30 today, personally, it may be too expensive for me to pick up some shares. Therefore, I will definitely add this solid blue-chip bank to my watchlist and wait before I nibble up some shares.

Disclosure: No position in DBS.

You can check out our latest articles here: Mastercard, ETFs and new Webull Referral.

Disclaimer: The information provided by LearnToInvest serves as an educational piece and is not intended to be personalised investment advice. Readers should always do their own due diligence and consider their financial goals before investing in any stock.

Comments

276

0

ABOUT ME

Singaporeans seeking FIRE by the age of 45

276

0

Advertisement

No comments yet.

Be the first to share your thoughts!