Advertisement

OPINIONS

Maximise Your CPF Ordinary Account for Higher Returns

CPF Ordinary Account lets Singaporeans grow spare cash safely with guaranteed interest.

This post was originally posted on Planner Bee.

When it comes to growing your savings in Singapore, most people immediately think of fixed deposits, robo-advisors, or high-yield savings accounts.

There is, however, another option that does not get enough attention, your CPF Ordinary Account (OA). This is the account where your monthly CPF contributions are deposited. With the right strategy, your OA can serve as a low-risk way to earn higher returns.

In this article, we unpack what makes the CPF OA appealing, why it can be a smart strategy for long-term savers, and how to decide if it suits your financial goals.

What is CPF OA and why it pays more than most bank accounts

The Central Provident Fund (CPF) is Singapore’s mandatory social security savings scheme for retirement, housing, and healthcare. Your monthly contributions are split between three accounts: the Ordinary Account (OA), the Special Account (SA), and the MediSave Account (MA).

The OA is the most flexible. It can be used for housing, education, and approved investments. The key advantage is the interest. The base rate is 2.5% per annum, and you can earn up to 3.5% on the first S$20,000 if you’re below 55, thanks to extra government interest.

High-yield savings accounts typically offer 0.05% to 3.0% p.a. and often come with conditions, such as salary crediting or spending requirements. Compared with that, CPF OA can be very attractive.

Why CPF OA can act like a high-yield account

The appeal of the OA lies in its steady interest rate, government guarantee, and zero market risk. While the funds are meant for housing or education, you can top up your OA voluntarily, and this is where it becomes a useful strategy.

By parking spare cash to your OA, you earn a reliable interest rate regardless of the economy. Unlike bank accounts, CPF interest has stayed stable over the years, making it a dependable option for long-term savings.

Interest is compounded and credited annually based on monthly balances. The earlier you top up, the longer your money can grow.

When it makes sense to park spare cash in your OA

This is not suitable for an emergency fund or money you might need soon. CPF funds are not as easily accessible as a bank account, so this strategy is only for cash you are confident you will not need for a long time.

You might consider adding spare cash to your OA if:

- You already have 6 to 12 months of emergency savings.

- You do not need the money till either upon a property purchase or retirement.

- You want a low-risk way to earn higher interest on idle cash.

- You are saving for a home and want to earn interest while waiting.

- You want to reduce mortgage debt by making partial repayments from your OA, earning interest until you use the funds.

Life stages and financial goals where this strategy works best

Who benefits most from this strategy? It depends on your stage of life and your financial priorities.

1. Young working adults without property commitments

If you’re in your 20s or early 30s, still renting or living with your parents, and not planning to buy property anytime soon, you can use your OA to accumulate interest while saving for a future flat.

An added advantage is that funds in your OA can later be used for your HDB downpayment or to reduce your mortgage loan.

2. Couples planning a home in a few years

If you plan to buy a BTO but are still a few years from key collection, you can transfer some of your spare cash into your OA instead of leaving it in a low-interest savings account. This allows your money to grow while you wait.

3. Parents who’ve paid off their home

Once your mortgage is cleared and your kids’ education is funded, but you are still earning, it is a prime time to channel spare funds into CPF. The OA interest can effectively supplement your retirement savings or contribute towards the Enhanced Retirement Sum (ERS).

4. Mid-career individuals with a cash surplus

If you are in your 40s or 50s and have built up a significant cash buffer, CPF offers a stable, passive growth option. It provides guaranteed interest without the ups and downs of market investments.

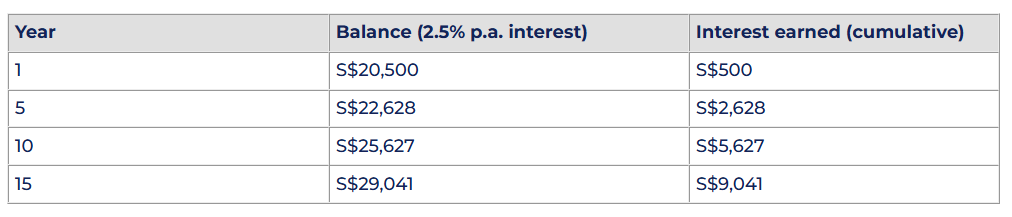

Potential interest earnings

For example, if you voluntarily top up S$20,000 into your CPF OA:

With compounding, topping up your OA could earn nearly S$13,000 in interest over 20 years, all without taking on investment risk.

If you qualify for the extra interest (up to 3.5%), your returns could even be higher. For those comfortable with a long-term lock-in, this is an attractive option.

Read more: How CPF Interest Rates Can Help Grow Your Money

Risks and limitations

This strategy is not suitable for everyone. Consider the following before contributing:

Lack of liquidity

Once you top up your OA, the funds are not easily accessible. It is not suitable for emergencies, travel, or short-term spending.

Property implications

If you plan to buy a home using your CPF OA, topping up too much could limit your flexibility for home loan cash flow, particularly if your property plans change.

Opportunity cost

If you are comfortable with investment risk, other instruments such as ETFs or S&P 500 funds may offer higher long-term returns, though they come with volatility.

One-way contribution

Voluntary CPF contributions are irreversible. Unlike cash, these funds are locked until you reach the eligible withdrawal age or use them for housing.

Read more: Investing Your CPF Savings: Is It Worth Putting Them in a Fixed Deposit?

Alternative CPF strategies

You can explore other ways to make your CPF work harder:

1. Transfer from OA to SA for higher interest

If your goal is retirement, transferring OA funds to SA can give 4% to 5% interest. This is irreversible but increases compounding power.

2. Top up SA via CPF Retirement Sum Topping-Up (RSTU) scheme

You can top up your SA or a loved one’s SA to build retirement savings and enjoy tax relief of up to S$8,000 per year.

3. Use OA to pay off your housing loan early

Excess OA funds can be used for partial repayments. This reduces your principal, saves on long-term interest, and offers peace of mind.

4. Invest with CPF OA via CPF Investment Scheme (CPFIS)

If you have a higher risk appetite, you can invest OA funds in stocks, ETFs, or unit trusts. Ensure your returns exceed the guaranteed 2.5% CPF interest.

Read more: Preparing For Retirement: How to Maximise Your CPF Savings

Making CPF work for you

The CPF OA is one of the most underappreciated financial tools available to Singaporeans. When used strategically, it offers a safe and reliable way to grow your wealth over the long term, thanks to guaranteed interest and the power of compounding.

This strategy is best suited for spare cash rather than funds needed in the short term. Make sure you have a sufficient liquidity buffer before committing idle money, and approach it with a long-term mindset to maximise its benefits.

Read more: Key CPF Changes in 2025 and How They May Affect You

Comments

40

18

ABOUT ME

Your Personal Mobile Financial Advisor Application Join us at telegram! https://t.me/plannerbee

40

18

Advertisement

No comments yet.

Be the first to share your thoughts!