Advertisement

OPINIONS

Best Bank Fixed Deposit Rates in Singapore for Savers

Fixed deposits remain a low-risk way to earn guaranteed interest on savings, though rates and terms vary across banks.

This post was originally posted on Planner Bee.

Looking for a safe and steady way to grow your savings?

Fixed deposits are still a popular choice in Singapore, especially for those who want guaranteed returns without taking on market risk. Although rates have fallen over the past year, local banks continue to offer competitive rates, even as global interest rates begin to cool.

Whether you are saving for the short term or prefer to lock in for longer, this guide highlights the latest fixed deposit promotions from major banks in Singapore. It covers key rates, tenures and terms so you can choose the best option for your needs.

What is a fixed deposit?

A fixed deposit (FD) is a savings product offered by banks where you place a lump sum of money for a set period at a fixed interest rate.

You typically earn more interest than a regular savings account because your funds remain locked in for the agreed tenure, which can range from one month to several years.

The returns are guaranteed and do not change with market movements, making FDs a low-risk option for cautious savers. You can withdraw early if needed, but this may reduce the interest earned.

In Singapore, fixed deposits are considered safe as they are offered by regulated financial institutions with clear terms and guaranteed returns.

Pros and cons of fixed deposits

Fixed deposits are reliable, but like any financial product they have both benefits and drawbacks.

Pros:

- Predictable interest and low risk

- No need for active management

- Suitable for short to mid-term savings

- Ideal for conservative savers

Cons:

- Limited liquidity as early withdrawals incur penalties

- Locked-in rates may lag if interest rates rise

- Returns may be lower after maturity if rates fall

- Higher rates often require fresh funds or meet certain minimum amounts

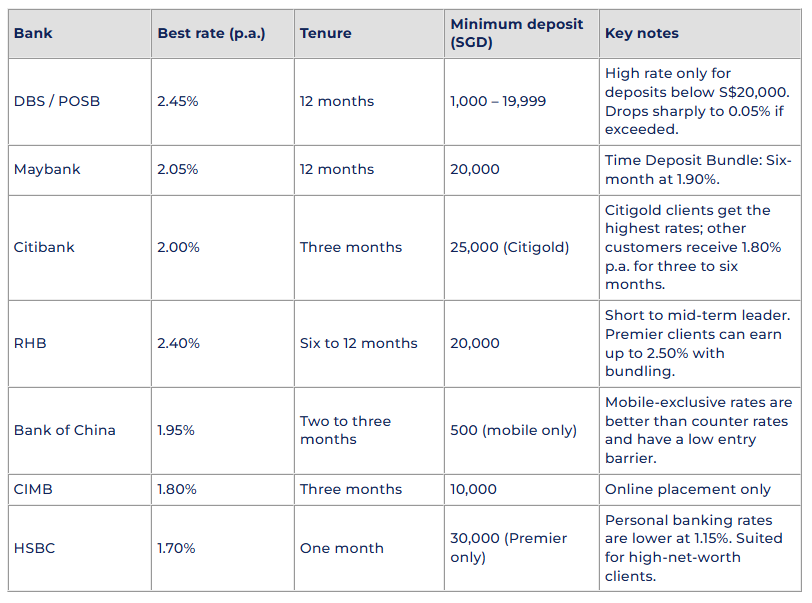

DBS / POSB

DBS and POSB are currently among the banks offering some of the best fixed deposit rates.

Their top rates include 2.15% p.a. for a six-month tenure and 2.45% p.a. for a 12-month tenure. These rates apply only to deposits between S$1,000 and S$19,999.

If your deposit exceeds S$20,000, the interest rate drops sharply to as low as 0.05% p.a. Splitting your savings into smaller deposits may help you get better returns.

Senior citizens with a DBS Premier Income Account (PIA) can also enjoy an additional 0.10% p.a. on top of the prevailing board rate.

Maybank

Maybank remains a competitive option for mid-term fixed deposits, although its promotional rates have eased in recent months.

As of July 2025, Maybank offers 2.05% p.a. for a 12-month tenure and 1.90% p.a. for a six-month tenure. Both options require a minimum deposit of S$20,000 under Maybank’s Time Deposit Bundle Promotion.

For savers seeking a balance between reasonable returns and shorter lock-up periods, the six-month placement is a practical low-risk choice, though rates are no longer at the earlier peak of 2.45% p.a.

Citibank

Citibank continues to focus its fixed deposit promotions on wealth clients.

Citigold customers enjoy promotional rates of 2.00% p.a. for a three‑month SGD time deposit and 1.90% p.a. for a six‑month tenure.

For regular customers across Citibanking, Priority, and Citi Plus, the board rate is 1.80% p.a. for both three and six-month tenures. These offers underline Citibank’s focus on providing enhanced returns for customers with shorter investment horizons.

RHB Bank

RHB Bank remains to provide competitive short-term fixed deposit rates. Effective 3 July 2025, the ordinary SGD time deposit rates are:

- Three to five months: 2.30% p.a.

- Six to 11 months: 2.40% p.a.

- 12 months: 2.40% p.a.

The minimum deposit requirement is S$20,000 across all tenures. Deposits can be placed online or over the counter, depending on the promotion. RHB is a good option for those seeking short‑term, high‑yield placements, particularly existing RHB Premier customers.

Read more: How Does Inflation Affect Your Bank Balance?

Bank of China (BOC)

Bank of China offers flexible fixed deposit options that appeal to short‑term savers. As of now, mobile banking placements earn:

- One‑month tenure: 1.80% p.a. (minimum deposit S$500)

- Two and three‑month tenures: 1.95% p.a.

- Six‑month tenure: 1.85% p.a.

- 12‑month tenure: 1.75% p.a.

Counter rates are lower and require a minimum deposit of S$20,000, with rates ranging from 1.60% to 1.75% p.a. These mobile‑exclusive promotions make BOC an attractive choice for those who want to park smaller amounts of idle funds for short periods.

CIMB Bank

CIMB continues to compete in the short- to mid-term fixed deposit market with online-exclusive rates. Its current three-month fixed deposit pays 1.75 % p.a. for Personal Banking customers and 1.80 % p.a. for Preferred Banking, both with a minimum deposit of S$10,000.

Although rates have slipped from earlier highs, these placements remain relatively competitive. CIMB’s online‑only promotions are particularly convenient for digital‑savvy savers.

HSBC

HSBC’s fixed deposit promotions largely cater to Premier clients with larger wealth holdings.

Premier customers enjoy 1.70% p.a. for a one‑month tenure, with a minimum deposit of S$30,000 in fresh funds. Personal banking customers receive lower rates of 1.15% p.a for one-month placement and 1.05% p.a. for three and six-month tenures.

HSBC’s fixed deposit rates are generally less competitive unless you qualify as a Premier client, but they may still appeal to customers who prefer to consolidate their wealth with one global bank.

Key factors to consider when choosing a fixed deposit

When choosing a fixed deposit, it’s important to look beyond the headline interest rate. Several factors can determine how well an FD aligns with your financial goals:

- Tenure and liquidity: Choose a time frame that fits your cash flow needs and goals. Shorter durations provide more flexibility if you need access to funds.

- Interest rate: Compare promotional and board rates, as these can change frequently.

- Minimum deposit: Requirements vary widely. Some banks accept as little as S$500, while others require tens of thousands

- Deposit source: Many banks only offer promotional rates for fresh funds.

- Placement channel: Online rates are often better than in-branch offers, but not always.

- Customer tier: Preferred, Citigold or Premier customers usually enjoy higher rates.

- Renewal policy: Be mindful of auto-renewals, which may default to lower board rates rather than the initial promotional rate.

By weighing these considerations carefully, you can choose a fixed deposit that balances security, flexibility, and returns.

Fixed deposit promotions overview

Fixed deposits remain a reliable option for those seeking guaranteed returns with minimal risk. While the headline rate is important, it is equally crucial to consider factors such as tenure, minimum deposit requirements, customer tier and renewal policies before committing.

The market is competitive, and promotional rates change often. Reviewing offers regularly and matching them to your savings goals can help you secure better returns. Whether you are saving for the short term or looking for a longer lock-in, there are options to suit different needs and risk appetites.

Read more: Getting Started With Fixed Deposits in Singapore: A Guide for Beginners

Comments

118

20

ABOUT ME

Your Personal Mobile Financial Advisor Application Join us at telegram! https://t.me/plannerbee

118

20

Advertisement

No comments yet.

Be the first to share your thoughts!