Advertisement

OPINIONS

Are Short Duration Bond Funds Worth It

Short-duration bond funds offer higher returns than deposits with modest risk and good liquidity.

This post was originally posted on Planner Bee.

With fixed deposit (FD) rates falling across Singapore, many investors are asking where they can park their savings for better returns without taking on too much risk.

One option that has become increasingly popular is short-duration bond funds.

These funds can offer higher yields than traditional FDs or T-Bills while maintaining relatively low volatility and providing flexibility for investors who may need liquidity.

This guide explains how short-duration bond funds work, how they differ from other low-risk investments in Singapore, and what investors should consider before adding them to their portfolios.

Why are Singaporeans turning to bond funds?

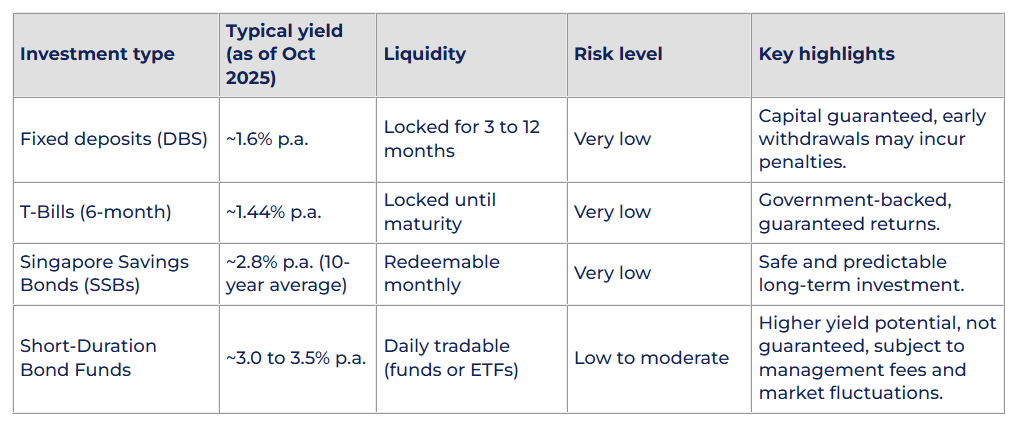

In the current low-interest-rate environment, traditional safe havens like T-Bills, FDs, and Singapore Savings Bonds (SSBs) have seen yields decline.

Recent examples include:

- The 6-month T-Bill auction on 9 October 2025 recorded a cut-off yield of 1.44% p.a., compared to 3.87% p.a. two years earlier.

- A 12-month fixed deposit from major banks such as DBS offers around 1.6% interest for deposits under S$20,000.

- The CPF Ordinary Account earns 2.5% interest, but funds are tied up and cannot be easily withdrawn.

In contrast, short-duration bond funds in Singapore currently offer yields between 3% and 3.5% per annum, depending on the specific fund.

For investors who want higher returns than FDs or T-Bills but prefer to avoid stock market volatility, these funds can be an appealing middle ground.

What are short-duration bond funds?

Short-duration bond funds invest in short-term fixed-income instruments such as government securities, high-quality corporate bonds, and money market instruments, typically with maturities between one to three years.

These funds are actively managed, meaning fund managers adjust the bond portfolio based on market conditions, interest-rate trends, and credit quality to optimise returns and manage risks.

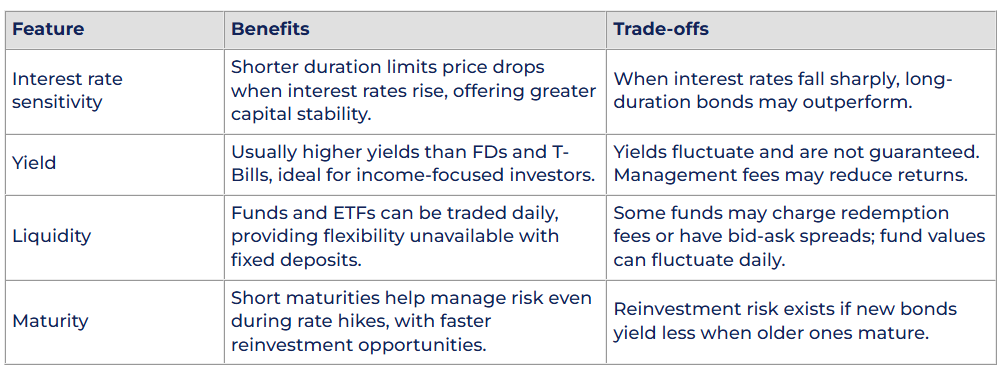

How short-duration bond funds work

Here’s how these funds operate and why they appeal to cautious investors in Singapore:

- Investment focus: They invest primarily in short-term bonds and money market instruments with stable income potential.

- Duration advantage: Shorter maturities help cushion price swings when interest rates change.

- Income generation: Bonds within the fund pay regular coupon interest, which is distributed to investors or reinvested.

- Liquidity: Most funds allow you to buy or sell daily through fund platforms or ETFs listed on the Singapore Exchange (SGX).

- Accessibility: Minimum investment amounts are typically low, sometimes as little as S$100, making them suitable for retail investors.

Core features, benefits, and trade-offs

Why they matter

In Singapore’s low-interest-rate environment, short-duration bond funds provide a practical balance between return, risk, and flexibility. They’re a strong fit for investors who:

- Want better yields than FDs or T-Bills

- Have low-to-moderate risk tolerance

- Value liquidity and professional management

- Don’t need the funds immediately

Before investing, review the fund’s factsheet, check its duration, yield-to-maturity, and credit quality, and ensure it aligns with your goals.

Read more: Are You Risk-Averse? Here Are 5 Safer Investment Options

Short-duration bond funds vs. T-Bills and fixed deposits

Traditionally, Singaporeans view T-Bills, fixed deposits, and Singapore savings bonds as safe investment options. However, with current yields barely keeping up with inflation, many are exploring short-duration bond funds for higher potential income.

A 12-month fixed deposit with DBS Bank for amounts under S$20,000 currently offers around 1.6% interest.

In comparison, short-duration bond funds in Singapore often deliver 3.0% to 3.5% p.a., depending on their holdings and management fees.

T-Bills and SSBs are guaranteed and low-risk, ideal for investors who dislike volatility. Short-duration bond funds, on the other hand, offer flexibility, higher yield potential, and daily liquidity, but come with credit risk and management costs.

Read more: Getting Started With Fixed Deposits in Singapore: A Guide for Beginners

Examples of short-duration bond funds in Singapore

- Amova Short Term Bond Fund (formerly Nikko AM)

- Objective: Preserve capital and liquidity while outperforming the Singapore Overnight Rate Average (SORA).

- Portfolio: Diversified short-term bonds and money market instruments.

- Stats (as of 30 June 2025): Weighted average duration: 1.61 years Weighted average yield-to-maturity: 3.57%

- Minimum investment: S$100

- Investment options: Cash, SRS, CPF OA / SA, or Regular Savings Plan (RSP).

- LionGlobal Short Duration Bond Fund (Active ETF – SGD Class)

- Singapore’s first actively managed short-duration bond ETF.

- Listed on the Singapore Exchange (SGX) for as low as S$1 per unit.

- Stats: Weighted duration: 2.17 years Weighted yield-to-maturity: 3.18%

- Management fee: 0.25% p.a.

- Investment options: Cash or Supplementary Retirement Scheme (SRS).

- Risk note: Includes exposure to sub-investment-grade securities, though actively managed to reduce credit risk.

Should you invest in short-duration bond funds?

Short-duration bond funds serve as a middle ground between low-yield safe assets (like FDs and T-Bills) and riskier investments (like equities). They are best suited for:

- Conservative to moderate investors seeking better returns than deposits.

- Those who don’t need immediate access to their funds.

- Investors willing to accept mild price fluctuations in exchange for higher income potential.

Pros

- Higher yield potential than traditional deposits.

- More liquid than long-term bonds.

- Lower sensitivity to interest rate changes.

- Professionally managed portfolios.

Cons

- Returns are not guaranteed.

- Subject to management and platform fees.

- Exposed to credit and reinvestment risks.

Final thoughts

Short-duration bond funds are becoming a compelling alternative for Singaporeans seeking stable yet flexible income options.

They strike a balance, offering better yields than FDs, T-Bills, and SSBs, while limiting exposure to market volatility. However, these funds are not risk-free and are most suitable for investors who understand and can accept moderate fluctuations in value.

Before you invest:

- Compare funds by yield, duration, and credit quality.

- Understand the fees involved.

- Ensure the fund aligns with your financial goals and risk profile.

Short-duration bond funds can be a valuable addition to your investment portfolio, but always do your own research before diving in.

Read more: Understanding the Power of Compound Interest

Comments

25

6

ABOUT ME

Your Personal Mobile Financial Advisor Application Join us at telegram! https://t.me/plannerbee

25

6

Advertisement

No comments yet.

Be the first to share your thoughts!