Anonymous

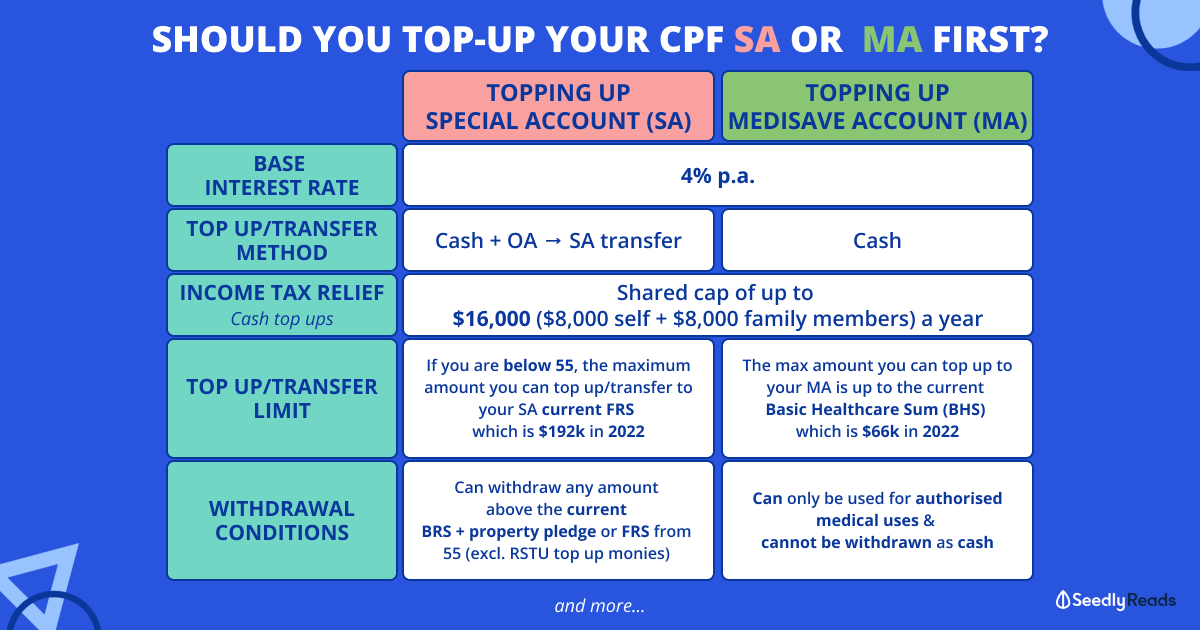

For salaried employees, why does one do a top up to CPF SA? Especially if the cash could be used to possibly generate a higher growth via investments?

I am 28 this year. Was thinking that with my current income, and assuming no increment, I could minimally reach BRS at my retirement age and possibly near FRS. Monthly payout for FRS to me looks reasonable so why do people still top up SA when payouts of such top ups is only through the annuity?

10

Discussion (10)

Learn how to style your text

Reply

Save

Quite a few answers provided, so I will jump straight into my perspective.

1) I am aiming for ERS that provides the most cash after I start cpf life payout. Its not that hard to achieve FRS, but there is some difficulty in compounding SA to achieve ERS through the SA balance alone.

2) why ERS? I estimate FRS would provide less than 2k equivalent (in today's dollars) while ERS would provide 2.5 to 3k equivalent when I want to start to draw down on cpf life payout. I am not quite sure that I can live on 2k monthly. I would like to aim for 5 to 7k monthly and so ERS will form the base for half the cash (or less) , and remainder from my investments (be it interests / dividends / selling).

3) risk free 4% is very difficult to beat consistently. I would prefer to diversify and spread my bets between cpf and equity.

4) yes stocks (or S&p specifically) seems to have a good growth rate that compounds exponentially. But there are market cycles, and if you were to depend on it alone, a sudden black Swan like covid could seriously dampen the amount you can draw down for that year. I would rather not risk a life that are good in some years, but absolutely horrible in the down years in retirement.

5) I am thinking of leaving some portion of my investments as a legacy so I would prefer not to touch or count on liquidating it unless I really have to.

As a concluding summary, it's not a one or the other decision path, but employing both would increase the likelihood of a more stable cash flow for me in my retirement years.

Reply

Save

That is because they believe in ah gong too much. The SA is a 30 year bond with no guarantee of redemption due to policy risk and a yield that does not reflect this risk accordingly

Reply

Save

I have been working for 30 years and began saving/ investing seriously when I hit 30. I have to say that up to 5% risk-free interest that you can earn on your SA is very hard to beat. Plus you can tax relief for the top-up. Only catch is that you can't touch your CPF savings until you hit 55.

Reply

Save

Kevin

24 Oct 2020

Mechanical Engineering at Nanyang Technological University

I'm with Shengshi on this one. The base line is that, if you believe you can grow your investable ca...

Read 6 other comments with a Seedly account

You will also enjoy exclusive benefits and get access to members only features.

Sign up or login with an email here

Write your thoughts

Related Articles

Related Posts

Related Posts

When you do top up, you get tax rebate too. Next is SA account get 4 to 5 percent interest, and is interest on top of interest. Risk free.

To get 4 to 5% return for investment, it is consider as mid to high risk already. Why take the risk especially when the market is uncertain at this time?